1. The NVIDIA Shiver and the Ghost of 1999

On January 27, 2025, the market suffered a localized seizure. NVIDIA—the high priest of the generative AI boom—saw its market capitalization crater by 17% in a single day. The resulting $600 billion loss set a grim record for the largest single-day value destruction by any company in U.S. stock market history.

The catalyst wasn’t a standard earnings miss. It was the release of DeepSeek R1—a low-cost, open-source model from China that suggested the “silicon moat” might be far shallower than investors had priced in.

{kind=link}

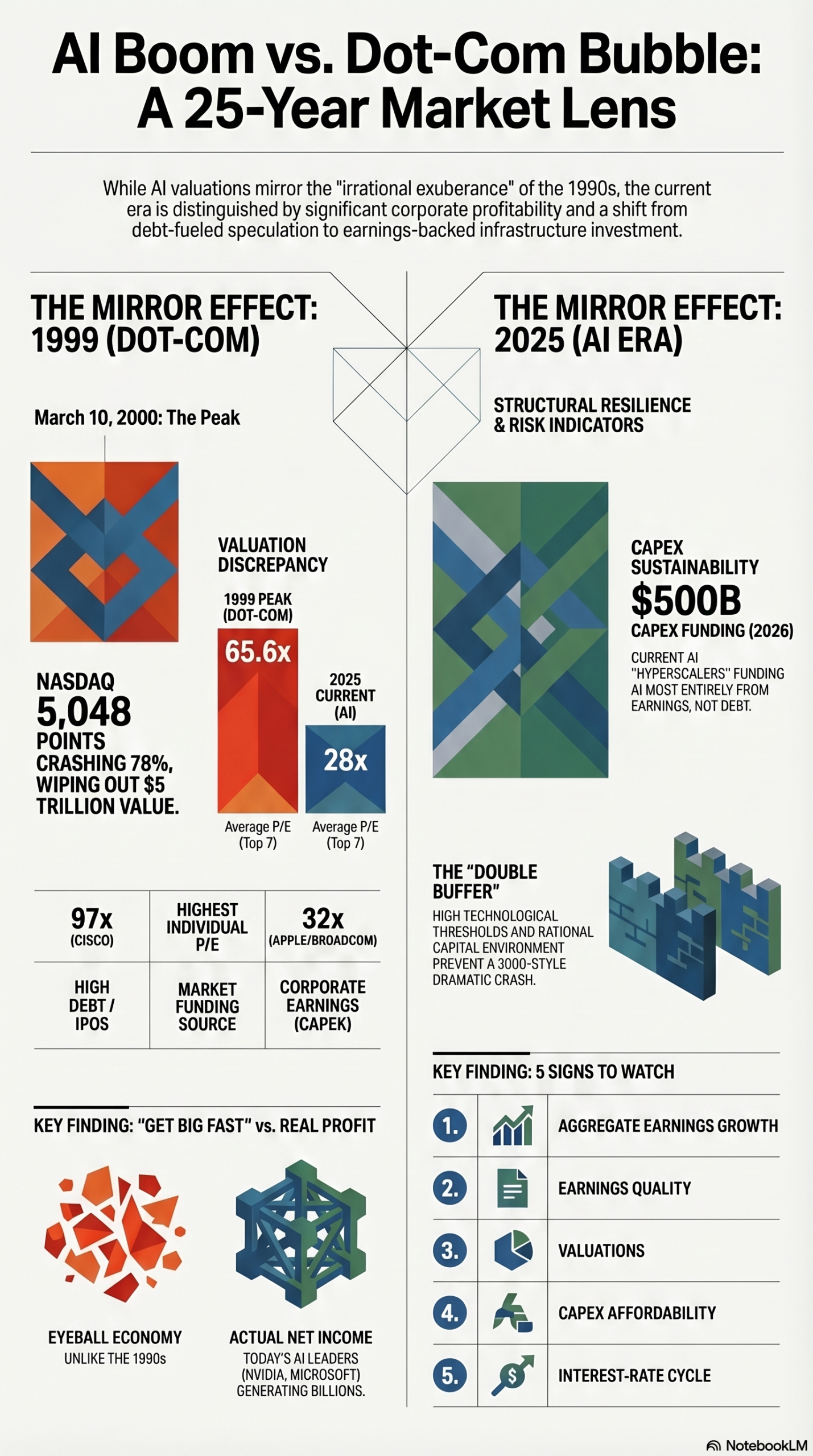

For the tech historian, this “NVIDIA Shiver” echoes March 10, 2000—the day the Nasdaq peaked before a two-year slide wiped out $6.5 trillion.

Curiosity has now evolved into something more urgent:

Are we standing on the edge of a dot-com-style collapse, or entering a necessary purification phase?

To answer that, we must distill 25 years of market mechanics—separating structural revolution from speculative mania.

2. The Profit Paradox: “Eyeballs” vs. Real Earnings

The fundamental difference between today’s AI rally and the late 1990s lies in the anatomy of the balance sheet.

In the late ’90s, the “unprofitable but high-growth” model was revolutionary. Netscape’s 1995 IPO introduced the “growth-at-any-cost” philosophy, with an EBITDA margin of -28.11% and ROE of -26.14%. Investors abandoned earnings-based valuation in favor of the “eyeball economy.”

Today’s market leaders—the “Magnificent 7”—are the opposite. They are high-margin, cash-flow fortresses.

As of late 2025:

- Magnificent 7: ~28x forward earnings

- Top 7 stocks in 1999: ~65.6x forward earnings

Stretched? Yes. Comparable to 1999? Not even close.

“Current AI companies that don’t deliver real GDP growth—and don’t have real demand—will eventually crumble.”

— Satya Nadella, CEO of Microsoft

3. The DeepSeek Disruption: Engineering Over Compute

If Netscape opened the door to the internet, DeepSeek R1 may have slammed the door on the “compute moat” era.

DeepSeek has turned the silicon moat into a footbridge—shifting the paradigm from:

- Capital-intensive AI → Efficiency-intensive AI

By reducing pre-training costs to less than 1/10th of industry norms, it dismantles the idea that dominance belongs to whoever owns the most GPUs.

This is, in effect, “technological affirmative action”:

- Smaller firms can compete

- Developing nations can leapfrog infrastructure barriers

- Closed ecosystems lose their grip

The takeaway is clear:

AI advantage is shifting from hardware scale to engineering intelligence.

4. The Capex Safety Net: Spending Earnings, Not Debt

The 2000 crash was fueled by debt-driven overcapacity. Telecom firms borrowed $500 billion to lay fiber no one needed—yet.

Today’s AI infrastructure is built differently.

Then (2000):

- Capex-to-Free-Cash-Flow ratio: ~4x

- Expansion fueled by debt

Now:

- Capex-to-FCF ratio: <1x

- Expansion funded by internal cash flows

Hyperscalers are building data centers using their own profits—not junk bonds.

This isn’t a house of cards.

It’s a calculated capital allocation strategy by the most profitable companies in history.

5. The “Wrapper Economy” Warning

At the top, the Magnificent 7 look solid.

At the bottom? A different story.

Enter the “Wrapper Economy”—AI startups that are little more than thin SaaS layers built on foundational models like GPT-4.

This mirrors the late ’90s:

- Low barriers to entry

- Rapid commoditization

- Businesses built on rented land

History is clear:

Bubbles don’t destroy technology—they purify it.

The winners won’t be wrappers.

They’ll be companies building indispensable, defensible value.

6. The Survivor’s DNA: Amazon vs. Yahoo

The companies that survived the dot-com crash shared a specific DNA.

Amazon:

- Invested in infrastructure (logistics, AWS)

- Prioritized long-term dominance over short-term profits

Google:

- Focused on breakthrough tech (PageRank)

- Built a durable revenue engine (AdWords)

- Avoided IPO hype

Yahoo (the cautionary tale):

- Over-reliance on ads

- Missed key acquisitions (Google, Facebook)

- Strategic stagnation

Today’s AI leaders are trying to avoid Yahoo’s fate by building vertical integration:

- Healthcare

- Education

- Full-stack ecosystems

They don’t want to be features.

They want to be plumbing.

7. Circular Financing: The Hidden Leak

The most subtle risk in today’s AI boom is circular financing.

Here’s the loop:

- Hyperscalers (Amazon, Microsoft, Google) invest in AI startups

- Startups spend that money on cloud compute—from those same hyperscalers

Capital flows in a circle.

This creates a distortion:

- Demand appears stronger than it actually is

- Revenue is partially self-generated

If that loop breaks—due to regulation or sentiment shifts—

the weakest players (wrappers) collapse first.

That collapse could ripple upward, deflating perceived demand for chips and cloud infrastructure.

8. The 17-Year Hangover: Timing Is Everything

Here’s the uncomfortable truth:

Being right about technology doesn’t protect you from being wrong about timing.

In 2000:

- Cisco was essential infrastructure

- The internet did change the world

Yet:

- Cisco lost ~80% of its value

- It still hasn’t regained its inflation-adjusted peak

Even Microsoft—one of history’s greatest companies—took 17 years to recover.

The lesson:

Markets price timing, not just truth.

9. Conclusion: The Aftermath Builds the Future

A correction isn’t just possible—it’s inevitable.

The convergence of:

- Slower-than-expected commercialization

- Hype transitioning to real revenue

- Structural inefficiencies

…will force a reset.

But this isn’t 2000.

Today:

- Infrastructure is profit-funded

- AI is already delivering measurable value

- The foundation is real

Bubbles are not the end of revolutions.

They are the filter that refines them.

The dot-com crash gave us the modern internet.

The AI correction will likely give us hyper-automation infrastructure.