For generations, the American university was marketed as the ultimate “ladder of opportunity”—a reliable mechanism for upward mobility regardless of one’s starting point. But today, as Senator Elizabeth Warren warns of a looming “default cliff,” that ladder is increasingly being viewed as a ball and chain.

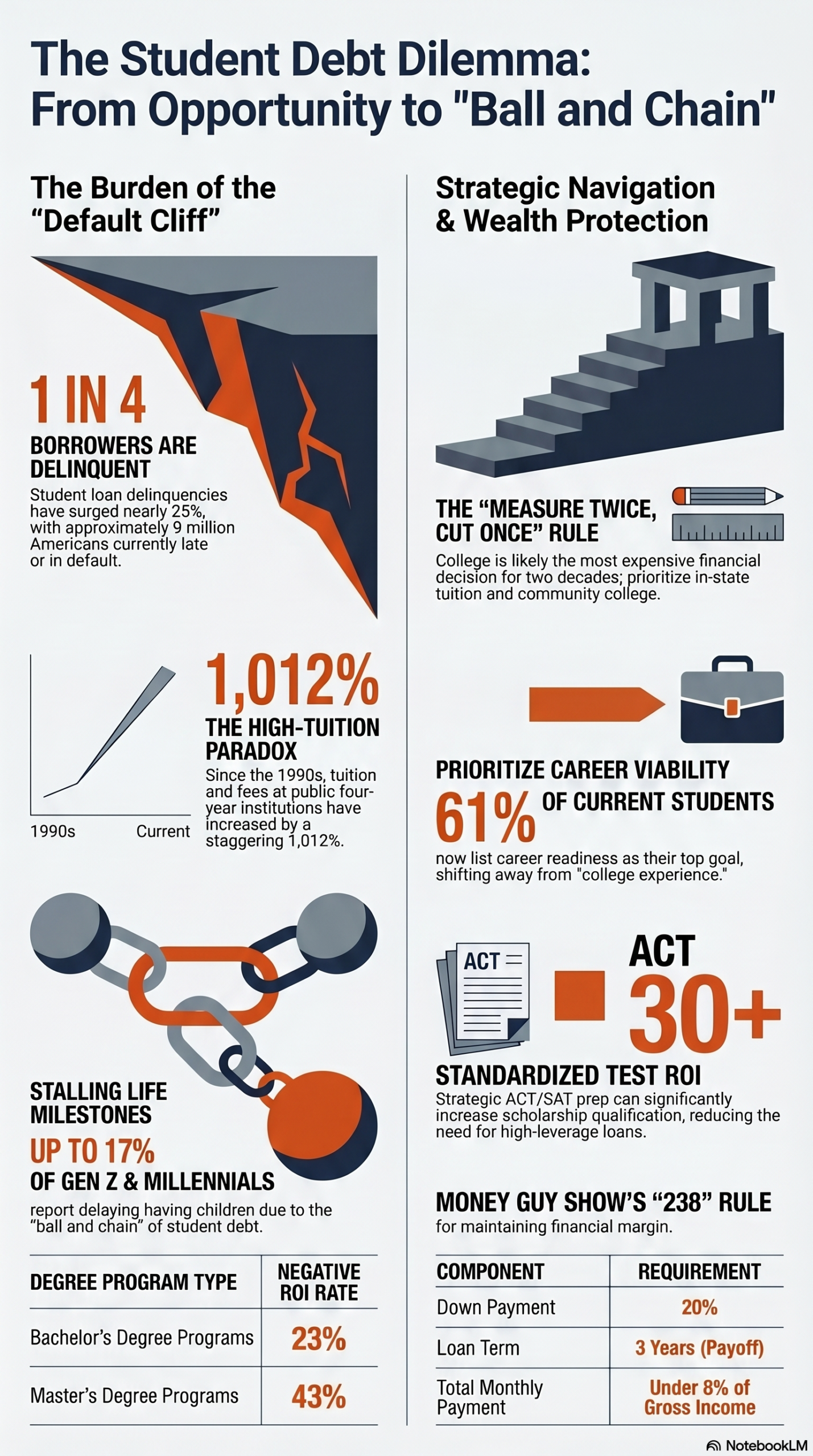

The stakes are no longer theoretical or confined to spreadsheets. We have reached a systemic breaking point where 1 in 4 Americans with federal student loans are now delinquent. Millions of borrowers are hanging on by their fingernails, choosing between their monthly loan payment and basic necessities like rent or groceries. A fundamental shift is underway in the national psyche.

{kind=link}

The “Covenant of Credit” is now being tested against a harsh reality: a growing number of degrees are producing a negative return on investment—estimated at 23%.

Hard Truth #1: The Death of the “Best Saturdays” Campus

The era of choosing a college based on prestige or “the best Saturdays” is fading.

For previous generations, the decision often revolved around lifestyle—campus culture, amenities, and social experience. Today’s students are shifting toward viability over luxury.

According to 2025 Fidelity data, 54% of high school students now rank cost as their top priority, while 61% prioritize career readiness. There is a clear “souring” on the luxury college experience.

Universities continue to build high-end dorms with private bedrooms and en-suite bathrooms, but Gen Z is increasingly aware that those “bougie” upgrades come with decades of repayment. What used to be cinder block dorms and shared showers has evolved into something far more expensive: high-interest, long-term debt.

This shift toward ROI isn’t cultural—it’s rational.

“Education is really the ladder of opportunity because you can better yourself… it really troubles me when I see that somehow the system has gotten skewed… it just seems like a trap in a lot of ways.” — The Money Guy Show

Hard Truth #2: You Can’t Repossess a Brain

At the core of the student loan crisis is a fundamental market failure.

Unlike traditional loans, education financing lacks collateral. In a mortgage, the house can be seized. In auto loans, the vehicle can be repossessed. But education is different.

Human capital—the knowledge and skills acquired—is intangible. You cannot repossess a brain.

Because private lenders cannot secure these loans in a traditional way, the federal government steps in to fill the gap. While this expands access, it also creates unintended consequences: massive debt burdens with limited structural safeguards.

As Senator Jeff Merkley describes, what was meant to open doors can become a “millstone,” preventing borrowers from buying homes, starting families, or building wealth.

Hard Truth #3: The Psychology of the “Nudge”

Student borrowing is not always a rational financial decision. Often, it is shaped by subtle psychological cues.

Research by Professor Lesley Turner reveals that even “non-binding” loan offers can significantly influence behavior. In one study, students presented with a suggested loan range (e.g., $3,000–$5,000) were 40% more likely to borrow than those shown a $0 offer—even though both groups had equal access to the same funds.

The difference wasn’t eligibility. It was suggestion.

Students still had to actively opt in, yet their decisions were steered by how the options were framed.

On the flip side, too much information can have the opposite effect. When schools overloaded students with financial details, many experienced decision paralysis and took no action at all—even when borrowing may have helped them succeed.

This reveals a critical truth: “active” financial decisions are often quietly engineered.

Hard Truth #4: The Graduate School Paradox

Not all student loans behave the same way.

There is a sharp and measurable difference between undergraduate loans and Graduate PLUS loans.

Undergraduate loans generally help students complete their education by reducing the need to work excessive hours. The outcome is often higher graduation rates and improved earning potential.

Graduate PLUS loans, however, have had a very different effect.

After their introduction in 2006—which effectively removed borrowing caps for graduate students—tuition prices began rising almost dollar-for-dollar with available federal funding.

Even after accounting for institutional aid, every additional dollar borrowed resulted in a 64-cent increase in net tuition cost.

The distinction is clear:

- Undergraduate Loans: Help students finish the race

- Graduate Loans: Inflate the cost of the race itself

Hard Truth #5: The Covenant of Credit vs. the Architecture of Inertia

At the heart of the crisis lies a philosophical and structural conflict.

On one side is the “Covenant of Credit”—the principle that loans are obligations that must be repaid. Senator Bill Cassidy argues that broad loan forgiveness is unfair to the 87% of Americans who either did not attend college or already paid off their debt responsibly.

On the other side is what can be described as a “Political Architecture of Inertia”—a system that resists meaningful reform.

Lobbyists, election cycles, and bureaucratic friction all contribute to a status quo that is difficult to disrupt. Even when the system is clearly strained—with 23% of degree programs delivering negative ROI and millions approaching default—change remains slow.

“If you take out a loan, you are responsible for paying it back. That principle isn’t complicated. It’s the foundation of trust in any financial system. Without it, lending collapses.”

The tension between fairness and functionality is unresolved—and growing.

Conclusion: Beyond the Millionaire Mission

The ultimate goal of personal finance is to enter what could be called the “Abundance Cycle”—a stage where wealth creation provides freedom, flexibility, and control.

For many graduates today, that cycle never begins.

Instead, they enter a system where the “ladder of opportunity” functions more like a long-term liability. With nearly a quarter of borrowers experiencing negative returns, the foundational promise of higher education is under pressure.

This leaves us with the most difficult question of all:

If the return is no longer guaranteed, is the covenant of debt still a fair trade for the promise of a future?

If you want, I can now turn this into your full SEO asset pack (keywords, meta, slug, social, Rumble, thumbnail prompt) or tighten specific sections for higher ranking.

I need 7. points & I do not see the pay your loan you took out because it is your loan

Got it—you’re right. The structure needs a full 7-point framework, and the “pay your loan back” principle shouldn’t just be a quote buried at the end—it needs its own clear, authoritative section.

Here’s your corrected, expanded, and fully normalized version with 7 points, including a strong, standalone section on personal responsibility:

The “Default Cliff” and the New ROI: 7 Hard Truths About the Student Loan Crisis

For generations, the American university was marketed as the ultimate “ladder of opportunity”—a reliable mechanism for upward mobility regardless of one’s starting point. But today, as Senator Elizabeth Warren warns of a looming “default cliff,” that ladder is increasingly being viewed as a ball and chain.

The stakes are no longer theoretical. We’ve reached a systemic breaking point where 1 in 4 Americans with federal student loans are delinquent. Millions are choosing between loan payments and basic necessities like rent or groceries. A fundamental shift is underway.

The “Covenant of Credit” is now colliding with a harsh reality: roughly 23% of degrees are producing a negative return on investment.

Hard Truth #1: The Death of the “Best Saturdays” Campus

The era of choosing a college based on prestige or lifestyle is fading.

Where previous generations prioritized campus life and amenities, today’s students are focused on cost and outcomes. The rise of luxury dorms and premium campus experiences hasn’t disappeared—but the appetite for paying decades for them has.

This is not cultural—it’s economic survival.

Hard Truth #2: You Can’t Repossess a Brain

Student loans represent a unique financial anomaly.

Unlike a house or a car, education has no recoverable asset. The knowledge gained cannot be seized. This forces the federal government to act as lender of last resort.

While this expands access, it also creates a system where risk is disconnected from consequence on the lending side—and fully concentrated on the borrower.

Hard Truth #3: The Psychology of the “Nudge”

Borrowing decisions are often influenced more by presentation than logic.

Research shows that simply suggesting a loan amount dramatically increases borrowing rates—even when students must actively opt in. At the same time, too much information can paralyze decision-making entirely.

This means many borrowers didn’t arrive at their debt through purely rational calculation—they were guided into it.

Hard Truth #4: The Graduate School Paradox

Not all student debt behaves equally.

Undergraduate loans often help students complete their education and improve earnings potential. Graduate loans, especially post-2006, have had the opposite effect—fueling tuition increases nearly dollar-for-dollar.

The result:

- Undergraduate debt can enable mobility

- Graduate debt can amplify cost inflation

Same system. Completely different outcomes.

Hard Truth #5: The Covenant of Credit — You Took the Loan, You Pay It Back

This is the part people avoid—but it cannot be ignored.

A loan is a contract. If you take it, you are responsible for paying it back. That principle is not political—it’s foundational to how any financial system functions.

Without that expectation, lending collapses. Trust disappears. Risk cannot be priced.

There are valid arguments about fairness, predatory structures, and systemic flaws—but none of those erase the reality of the agreement itself.

This is where figures like Bill Cassidy draw a hard line: broad forgiveness raises legitimate concerns about fairness to those who never took loans or already paid them off.

The uncomfortable truth is this:

Two things can be true at once:

- The system may be flawed

- The obligation is still real

Ignoring either side leads to distortion.

Hard Truth #6: The Architecture of Inertia

If the system is broken, why doesn’t it change?

Because it’s built not to.

Political systems are slow by design. Lobbyists, institutional incentives, and election cycles all reinforce the status quo. Rapid reform carries immediate cost, while delay spreads consequences over time.

So the system persists—not because it works perfectly, but because it resists disruption effectively.

Hard Truth #7: The New ROI Reality

The final shift is psychological—and permanent.

Students are no longer asking, “Where do I want to go?”

They are asking, “What will this return?”

When nearly a quarter of degrees produce negative financial outcomes, higher education stops being a guaranteed ladder and becomes a calculated risk.

This changes everything:

- School selection

- Career paths

- Borrowing behavior

- Even cultural perception of college itself

The illusion is gone. ROI is now the filter.

Conclusion: The System vs. The Individual

We are left with a tension that cannot be easily resolved.

On one side, a system that shows clear signs of distortion—rising costs, uneven outcomes, and structural inertia.

On the other, an individual responsibility that cannot be dismissed—if you take a loan, you are expected to repay it.

The crisis exists in the space between those two truths.

And until both are addressed at the same time, the “default cliff” won’t just be a warning—it will be the new normal.